Private Equity Pulse: key takeaways from Q3 2025

- tmgceo8

- Nov 26, 2025

- 5 min read

Private equity exits reach a three-year high, as firms seize opportunities to turn strategic value creation into realized returns.

In brief

Private equity activity surged in Q3 2025, with deal value reaching a record US$310b as firms leaned into a window of opportunity in the M&A markets.

While fundraising remains subdued, emerging retail channels and the gradual reopening of IPO markets signal a sector regaining momentum.

The third quarter of 2025 saw momentum continue to build amid rising sentiment, as private equity firms moved beyond the “cautious optimism” that defined the first half of the year and the transaction market largely shrugged off concerns around potential growth headwinds.

The rebound aligns with improving macro fundamentals — equity markets continued to climb through Q3, inflation moderated across most G20 economies and expectations for rate cuts in 2026 are firming. Against this backdrop, both sponsors and lenders appear increasingly comfortable underwriting larger, more complex transactions.

Overall, firms announced 156 deals in Q3, and the value of those deals — helped along by the largest announced leveraged buy-out (LBO) of all time – reached an all-time quarterly high of US$310b, as private equity sponsors (and the deal market at large) focused on fewer, larger transactions. Indeed, the quarter saw five PE deals broach the US$10b mark in Q3 — the same as the entire first half of the year.

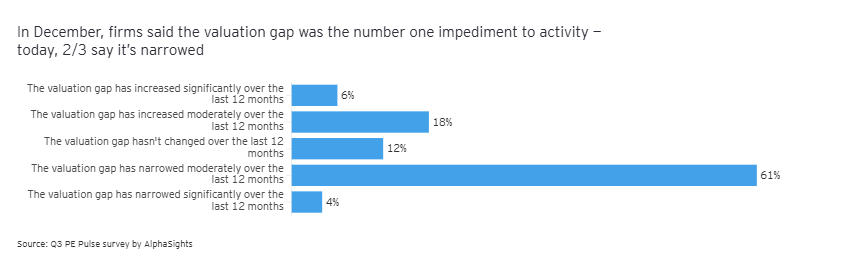

Bridging the valuation gap

For much of the past two and a half years, valuation mismatches have represented the greatest obstacle to dealmaking. As recently as last December, investors cited the valuation gap as the single largest impediment to transactions. Today, that barrier has meaningfully receded. In our latest global general partner (GP) survey, two-thirds of respondents report that the gap has narrowed, enabling buyers and sellers to find common ground and move forward with confidence.

At the same time, firms are increasingly deploying creative structures — such as earnouts, tariff-related material adverse change (MAC) clauses, and other contingent mechanisms — to mitigate risk and progress deals in uncertain environments. This flexibility has allowed sponsors to maintain transaction momentum even as long-term macro questions remain unresolved.

Financing conditions have also improved notably. Direct lenders remain highly active, offering competitive pricing and flexible structures, while the broadly syndicated loan market has reopened for larger buyouts. In the US, for example, syndicated loan activity surged to US$404b in Q3, the highest on record, according to Pitchbook LCD, underscoring the renewed confidence of both borrowers and lenders.

Sector reallocations underway

Q3 brought a measure of sector rotation, a shift that wasn’t unexpected given the tariff announcements earlier in the year. Investors responded by channeling more capital toward industries viewed as less exposed to trade frictions and more resilient to macro uncertainty.

Allocations to health care and financial services have more than doubled year to date and by contrast, technology — long the dominant destination for private equity capital — saw only a modest 5% rise in deployment compared with last year. The result is a clear pivot toward infrastructure, health and other essential services — sectors where stable demand and domestic exposure provide insulation against external shocks.

Exits tick higher as pressure continues to build

While not yet matching the record levels seen in deployment, exit activity accelerated meaningfully in Q3. Private equity firms have announced exits totaling US$470b so far this year — a 40% increase by value compared with the same period last year.

It’s a welcome development for an industry that has been holding assets longer than anticipated. With more than 30,000 PE-backed companies globally, pressure from limited partners (LPs) for liquidity continues to intensify. One year ago, roughly three-quarters of GPs rated LP pressure between five and seven on a 10-point scale. Today, the majority rate it between 6 and 8, underscoring that expectations around distributions have only grown stronger.

A promising trend has been the gradual reemergence of the PE-backed IPO market. After two years of muted activity, Q3 saw a number of high-profile listings come to market, together raising more than US$18b in aggregate proceeds. While modest compared with the pre-2021 boom years, these offerings are meaningful in signaling that public market investors are once again open to new issuance from PE portfolios. Notably, successful debuts have been concentrated in sectors with clear growth narratives and resilient earnings profiles, such as health care and financial infrastructure.

As fundraising slows, regulatory changes could yield meaningful longer-term tailwinds

As exit activity begins to show signs of life, attention naturally shifts to fundraising, where the environment remains more challenging. Through the first three quarters of 2025, private equity firms have raised approximately US$340b, putting the industry on pace for a roughly 25% decline versus last year. The slowdown reflects both a more measured pace of capital deployment by LPs and lingering caution around distributions.

However, recent changes to US retirement law allowing private equity and other alternatives to be included in 401(k) plans could provide a powerful new tailwind for capital formation. With roughly US$9t currently held in defined-contribution plans, even a modest allocation could translate into US$500 to US$600b of incremental flows into private markets over time.

Private equity firms are paying attention — in our latest survey, 90% of GPs say they’re at least “somewhat interested” in developing products for the defined contribution market. And a significant minority — 24% — report that they are already actively designing or developing such products.

A number of dynamics will define the pace at which adoption occurs, including the level of demand from plan sponsors, the need for additional regulatory clarity, scalable product structures and the need for operational infrastructure to support the rollouts. As these pieces come together, the inclusion of alternative assets in 401(k) plans, together with private equity’s push into other types of retail-oriented vehicles, could evolve from a nascent opportunity into one of the most significant drivers of industry fundraising in the decade ahead.

Outlook - GPs signal stronger activity ahead

In Q3, the percentage of firms expecting exit activity to increase surged from 44% to 61%, the highest level recorded since we began tracking GP sentiment more than two years ago.

That renewed confidence in liquidity marks a critical turning point, with sponsors more willing to bring assets to market and buyers demonstrating appetite for scaled opportunities.

Deployment expectations are equally encouraging. Three-quarters of GPs now anticipate deal activity will increase over the next six months, a seven-point jump compared with the prior quarter. This momentum is supported by narrowing valuation gaps, more creative structuring solutions, and improving alignment between buyers and sellers — tailwinds that collectively point to a stronger transaction pipeline heading into year-end.

Further evidence of a rebound is extant in firms’ stated hiring plans for the next 12 months.

According to our survey:

While risks remain — from tariffs to broader macro volatility — the market’s tone is clearly shifting. Sponsors, and transactors at large, now see a clear window of opportunity, leaning into a measured “risk on” posture that balances optimism with discipline. Capital is increasingly being directed toward transformational transactions and essential sectors that offer both growth potential and resilience.

Summary

In Q3 2025, private equity activity surged, achieving a record US$310b in deal value as firms capitalized on narrowing valuation gaps and renewed market confidence. With 156 deals announced, including six exceeding US$10b, the sector is pivoting towards larger transactions. Improved financing conditions and creative deal structures are facilitating this momentum. Looking ahead, 61% of firms anticipate increased exit activity, signaling a robust outlook as the market embraces a "risk on" approach, balancing optimism with discipline.

Comments